Top Misconceptions on the GHGP Scope 2 Updates

Ahead of the Greenhouse Gas Protocol (GHGP) publicly releasing the 1000+ consultation responses it received to its Scope 2 proposal survey, which concluded in January 2026, EnergyTag is addressing some of the most persistent myths surrounding the update. As the final standards take shape, stakeholders deserve an evaluation that is grounded in the truth, not misconceptions.

Myth #1: GHGP is a “24/7 mandate” that forces buyers to do 100% hourly matching

Factually incorrect. GHGP is a voluntary greenhouse gas accounting standard, not a target-setting organization or a regulatory body. It builds the carbon accounting framework; it does not dictate corporate procurement strategies. Confusing more transparent data tracking with an operational “24/7” mandate is a fundamental misunderstanding of what the proposed standard does. Any conflation of hourly accounting with “24/7 mandates” is incorrect.

Under current annual accounting rules, “100% clean” has become a misleading metric:

- Exaggerated claims: “100% clean” solar- or wind-only procurement is actually only about 40-60% clean on an hourly basis. Status quo annual accounting creates an illusion of perfection or completion, which is far from the physical reality.

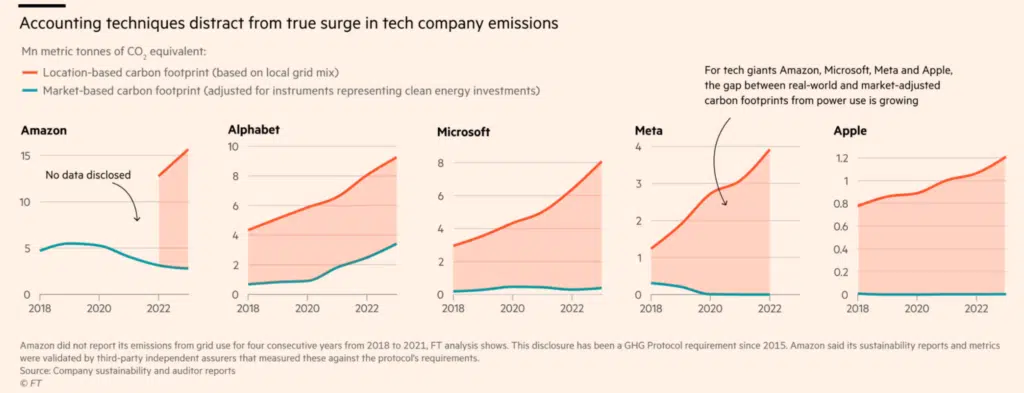

- Emissions decoupling: All four Big Tech companies are already “100% renewable” while simultaneously increasing their absolute grid emissions. Are they really “done”?

- Low attainment: While some companies make misleading “100%” claims allowed under existing rules, it’s also true that only about 20% of RE100 companies even report 95%+ renewable energy. 100% is not the only goal today, and it definitely won’t be under hourly matching either – true decarbonization is a journey.

- Lower-quality claims: A significant proportion of CDP-reported clean energy today relies on unbundled certificates rather than physical grid delivery.

Even under status quo annual accounting, “100%” is not required and is far from the only goal. The evolution towards hourly accounting is necessary to differentiate genuine procurement ambition from administrative compliance and provide decision-useful data. Put simply: 95% hourly matching means a lot more than 95% annual matching.

Source: Financial Times.

Myth #2: GHGP’s proposal will make clean procurement more expensive and difficult

Demonstrably false. Critics often rely on models that force immediate, full 100% hourly matching, which is indeed difficult and expensive at present. Because GHGP does not mandate targets, companies remain entirely free to scale their clean energy matching based on their budget and climate ambition.

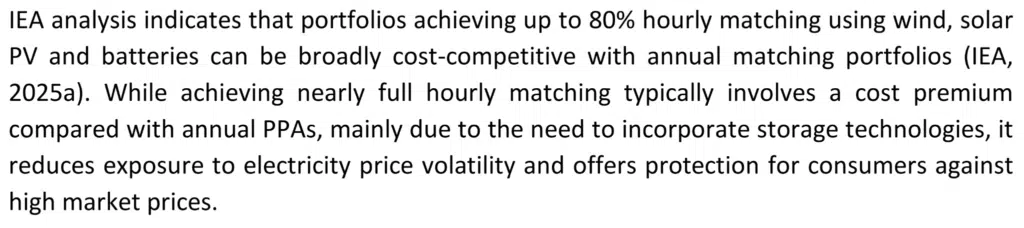

Furthermore, hourly matching is increasingly a sound financial strategy. High levels of hourly matching (80%+) can already be cost-competitive with industry retail prices and/or annual matching today. And they provide increased hedging value:

Source: IEA.

Updated rules therefore align with the clean power purchases companies already make for better hedging value & firmed clean energy supply. A fact being increasingly noted by portfolio managers & PPA experts. PPA expert Luca Pedretti of Pexapark summarizes it well, noting the real cost risks of annual matching and the imperative of more hourly-matched portfolios:

“The new additionality is raising your CFE [carbon-free energy] score above your country baseline; not matching consumption with GoOs or PPAs on an annual basis, which no longer provides an effective power price hedge either. Procuring with a CFE mindset will generate both economic and environmental value.”

While regional deliverability requirements may increase competition for clean supply in certain grids, this introduces an opportunity, not a problem: it incentivizes clean energy deployment everywhere the grid actually needs it, rather than continuing a race to the bottom to the cheapest, over-saturated markets (e.g., Texas in the US, or Norway’s glut of existing hydro certificates flooding the EU). And if companies “max out” what they are able to procure in-region, they do have the choice of outside-inventory procurement, the separate reporting of which is currently being standardized by the GHGP AMI working group.

The only cost impacts left to contemplate are therefore “operating costs” of one’s sustainability team and tracking, which Watershed estimates “could rise by low single-digit percentages relative to electricity spend.”

Myth #3: GHGP will invalidate companies’ existing procurements and ruin their targets

Highly unlikely. Critics frequently ignore GHGP’s extensive consideration of both legacy clauses to protect existing procurements and multi-year phase-ins of the new rules as a transition mechanism. The details of these provisions are important and could have implications for, say, a company’s 2030 Scope 2 target, but omitting these transition mechanisms’ existence misrepresents a well-planned phase-in period and stokes artificial panic.

Myth #4: Everyone must do hourly accounting, reducing participation from small orgs

Highly unlikely. GHGP has explicitly proposed exempting smaller organizations from hourly matching. Exemption criteria are being developed and may be based on a company’s electricity usage, company size, or some combination of those metrics. A large majority of companies would be exempt using any of the three proposed electricity usage thresholds. Exempt companies could continue to use annual or monthly accounting, while large organizations – which represent an outsized portion of electricity use and clean procurement – lead the way by accounting hourly first. This demand for hourly accounting will accelerate the growth of hourly accounting solutions that are already advancing today.

It is true that the proposal, as written, does not exempt anyone from the new deliverability rule. Some argue that this could use an exemption clause more than hourly accounting. GHGP is trying to strike a balance between its hierarchy of integrity, impact, and feasibility goals. We encourage stakeholders to engage thoughtfully on the program design of this still-draft standard.

Myth #5: Hourly matching is impossible without massive upgrades to data availability

Demonstrably false. Power markets run on (sub)hourly data, and even if a company does not have access to this data, hourly accounting can be layered on top of existing monthly/annual procurements – no new data or contract changes needed. Monthly utility bills can easily be converted to hourly data using common demand profiles, and even the simplest “flat-average” hourly demand profile assumption is more accurate than today’s annual accounting. Renewable generation profiles can similarly be layered on top of monthly/annual certificates if the underlying hourly data is not accessible. This can be done – and is being done – today.

Feasibility measures aside, natively-hourly data to the buyer is better and growing rapidly in availability worldwide. 46+ suppliers with hourly matching tariffs, growing 4x year-over-year. LevelTen funding five major certificate registries covering 70+ countries to upgrade to hourly granularity. Hourly certificates in Texas.

All of this is happening even before the GHGP has made their proposed updates. Granular accounting of clean procurements is the future, and accounting math is not the bottleneck – our conviction to progress forward against misinformed opposition is. If a bagel shop in Texas, data centres in Sweden, and people charging their EVs in Japan can do it, the largest companies in the world can and should do it, too. See 10+ TWh of case studies here.

Myth #6: Optional hourly accounting for everyone is enough of an improvement

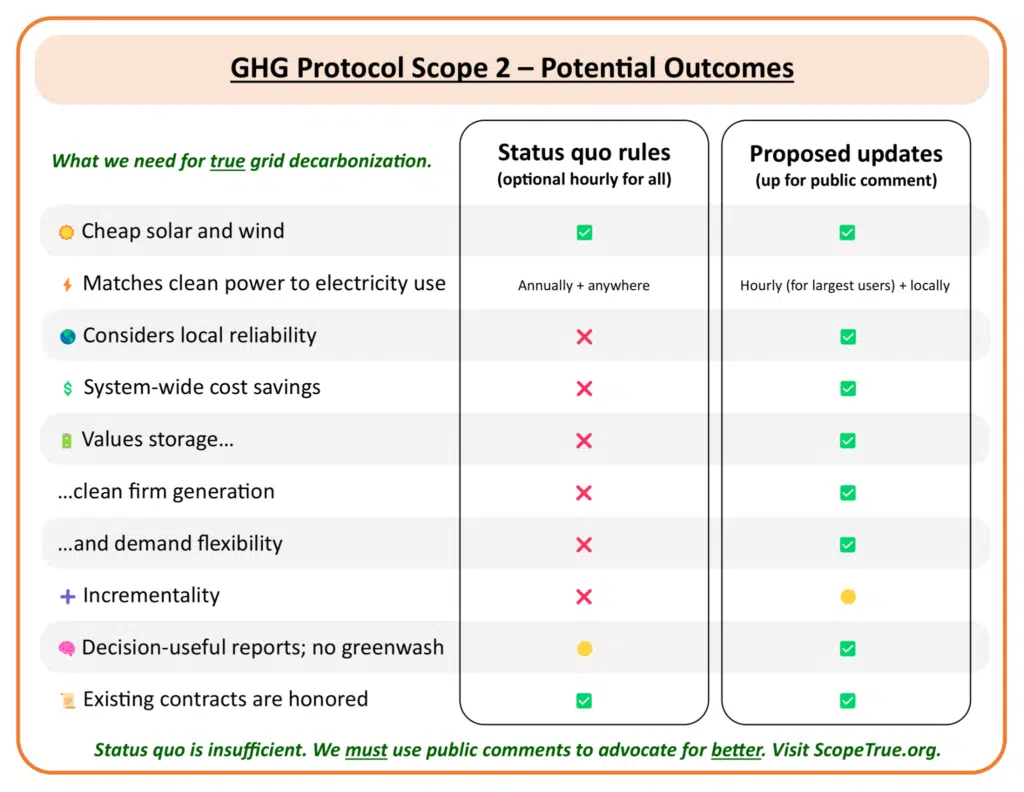

Demonstrably false. Broad coalitions have called for much-needed updates to GHGP accounting for years, including increased granularity in market-based accounting. Optional hourly market-based accounting for everyone (“may not shall”) is just the status quo, and retaining the status quo does not ensure specific integrity and impact. The original Scope 2 rules came out in 2015, and how we measured progress then should not be how we measure it in 2040, which this next iteration could last until. The status quo places zero value on storage and hardly incentivizes clean firm power or flexibility. With these technologies so critical to renewable integration, any standard ignoring or devaluing them is set for irrelevance. Evolution is natural and necessary.

Media coverage has repeatedly highlighted how out of date the status quo standards are. Other coverage has called out organizations like SBTi for considering weakening its standards and companies like Microsoft for considering weakening its climate targets. NGOs also publicly addressed these SBTi and Microsoft developments. GHGP must stay the course and enact the much-needed proposed updates – both for climate impact and their own legitimacy.

As the foundation of voluntary and regulatory reporting frameworks worldwide, the GHGP must meet the moment to encourage and enable true deep decarbonization and sustainability transparency. The proposed updates are a great step towards this; retreating to the status quo would be a huge integrity failure and a reputational implosion for the GHGP.

Myth #7: This will kill investments in renewables

Highly unlikely. The International Renewable Energy Agency (IRENA) had the following to say in their recent “24/7 renewables” report:

“The ongoing revision of the GHG Protocol Scope 2 Guidance proposes to extend this logic globally, requiring hourly and location-matched certificates as the basis for corporate market-based emissions claims. When adopted, this shift will transform demand for firm renewable electricity from a voluntary commitment by leading buyers into a mainstream feature of corporate energy procurement worldwide.”

Rather than depressing clean energy deployment, the proposed updates will strengthen corporate procurement by introducing critical time- and location-based investment signals that are currently missing from the rules. By aligning accounting with physical grid realities, the framework continues to heavily incentivize long-term PPAs while clearly identifying high-value opportunities for investment during the harder-to-decarbonize hours. For a deeper debunk of this myth, see our prior blog here: Scope 2 Updates Strengthen Clean Energy Markets. You can also check out our prior FAQ blog here co-signed by nine GHGP Scope 2 Technical Working Group members.