India’s Draft National Electricity Policy 2026: Signals a Shift in Power System Thinking

Shailesh, our Head of APAC, has spent some time going through India’s Draft National Electricity Policy (NEP) 2026 and has shared some of his thoughts below. It is still a draft, so many things can change. But when reading it fully, it feels like something more fundamental is happening. Not a big policy shift on the surface, but maybe a change in how the system is being thought about.

From Adding Capacity to Managing the System

For many years, the focus in India was clear – add capacity, expand access, and scale renewable energy. That made sense. The system needed more electricity, and solar and wind helped meet that demand at a lower cost.

However, we now have significant renewable capacity, but mismatches between supply and demand are becoming more visible. Solar peaks in the afternoon, while demand often rises in the evening. Wind also varies by season and location.

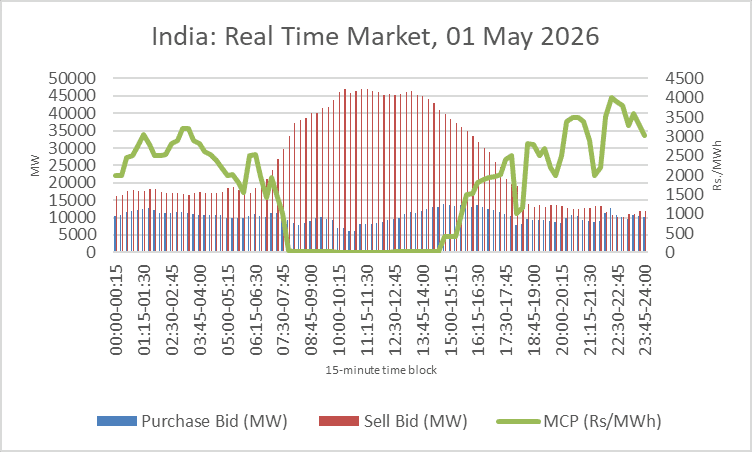

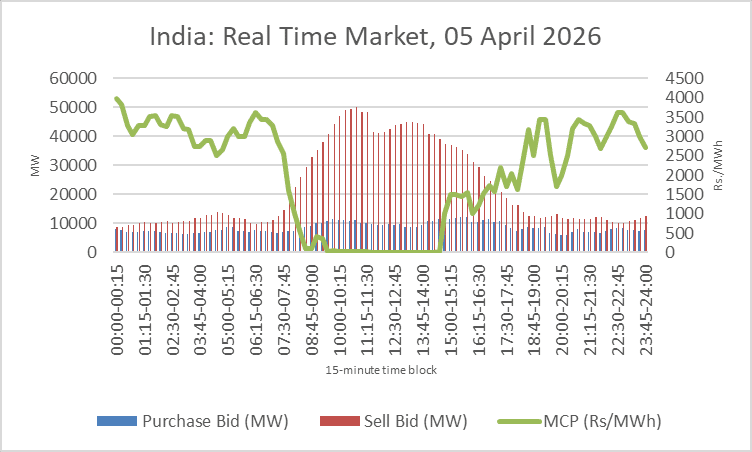

We are already seeing early signals of this. On 5 April and 1 May 2026, exchange prices fell to near zero during the afternoon hours. This was driven largely by peak solar generation and likely weather-driven reductions in demand. This points to a growing timing mismatch between when renewable electricity is generated and when it is needed.

Source: EnergyTag, based on IEX RTM data. Where MCP is Market Clearing Price: Final discovered market price for that time block.

Reading the draft NEP in this context, it feels like the focus is shifting from how much we generate to how the system behaves across the day.

Electricity Needs to Show Up When It’s Needed

Earlier, system planning was mostly based on energy. If enough units (kWh) were generated over a period, the system was considered adequate.

But in practice, operators were already dealing with timing issues, managing peaks, balancing variability, and ensuring supply during critical hours. These issues are being introduced more explicitly in policy.

The draft NEP talks about:

- hybrid RE + storage

- resource adequacy planning

- flexible operation of coal plants

Electricity is no longer just being treated as energy generation, but as a system that must reliably deliver power when demand exists.

Storage is No Longer on the Sidelines

In the earlier setup, storage was not a major part of the system.

Instead, mechanisms like banking were used. Renewable generators could inject power at one time and use it later. In a way, the grid was doing part of the balancing.

Now, this approach is slowly being reconsidered.

The draft NEP suggests:

- Gradual move away from banking.

- More storage at the consumer and system level.

- Introduction of concepts like “Cloud Energy Storage”.

- Stronger push for RE + storage combinations.

So, instead of the grid absorbing variability, the expectation seems to be that variability will be managed through assets such as storage.

Flexibility is Becoming More Visible

Earlier, flexibility was mostly handled inside the system.

Coal plants were adjusting output. Hydro was used for balancing. System operators were managing everything in real time. But these services were not always separately recognized or valued.

Now, this is starting to change.

The draft NEP mentions:

- Capacity markets to ensure the availability of capacity

- Expansion of ancillary services for grid stability

- Participation of demand response and aggregators

This suggests that flexibility, whether from generators, storage, or consumers, may become something that is more structured and possibly priced.

Contracts and Markets May Start to Come Closer

Traditionally, long-term PPAs in India were quite straightforward.

A generator signs a contract with a DISCOM or consumer. Power is scheduled based on that contract. The role of power exchanges was mostly for short-term balancing.

Now, there are early signals of change.

The draft NEP suggests that electricity from long-term PPAs may be routed through exchanges or recognized platforms. At the same time, open access and market-based procurement continue to expand.

This could mean that over time:

- Contracts may remain important

- But actual dispatch and settlement may increasingly interact with markets

- A more system-aware approach

Earlier, planning of generation, transmission, and distribution was often done in parts.

Large renewable projects were developed far from load centres. Transmission was built to connect them. Distribution managed local demand.

Now, the policy seems to be encouraging more integrated thinking.

There are references to:

- Developing RE (with storage) closer to the load

- Better use of existing transmission

- Integrating distributed energy resources

- Including demand-side participation

This suggests a shift toward looking at the entire system together, rather than optimizing each part separately.

What This Could Mean for Corporate Renewable Energy Procurement

In India, corporate renewable procurement, especially through open access, has mostly focused on cost. Companies typically sign solar or wind PPAs, use banking where available (to use the grid as a big battery), and rely on the grid to manage differences between generation and consumption.

This model has worked so far.

But we are already seeing early signs of change.

Round-the-clock (RTC) tenders have increased in recent years, especially for utilities. And similar ideas are now appearing in corporate procurement as well.

One example is the 100 MW RTC project developed by Ayana Renewable Power for Hindalco Industries Limited’s Odisha smelter. This project combines solar, wind, and pumped hydro to deliver a more stable and continuous supply, closer to the needs of an industrial load.

This is still a small share of the market.

But it shows a possible direction.

As storage becomes more important, and as system-level constraints become more visible, procurement may slowly move from only the lowest-cost energy to electricity that better matches when it is needed.

Looking Slightly Beyond India

India is not alone in this transition. Some of these signals are already visible in other markets. In Europe and California, high solar penetration has led to more frequent zero or negative prices during certain hours. This is not just a pricing issue; it shows that supply and demand are not aligned in time, and flexibility is limited.

The response has been quite consistent – more storage, stronger balancing markets, and greater use of demand-side flexibility. Simultaneously, growing trade-related requirements (e.g., CBAM) and evolving carbon accounting standards such as GHG-P Scope 2 require aligning electricity use with clean supply. This is also starting to influence how companies think about procurement.

A Quiet Transition

There is no big headline change in the draft NEP 2026. But there is a change of focus – t – from a system concentrated on how much electricity we generate, to a system that also focuses on how and when that electricity is delivered.

From an EnergyTag perspective, this direction feels familiar. Many of the themes emerging in the draft, including storage, flexibility, and system integration, naturally moving toward a power system where the timing of electricity starts to matter more.

This is often how power systems evolve as the share of renewable energy increases.