GHG Protocol Scope 2 Update: 7 Key Messages

The Greenhouse Gas Protocol (GHGP) is in the midst of a multi-year revision of its standards. A key part of this review is the update of the Scope 2 guidance — the rules that define how companies account for emissions from purchased electricity. If you’re working in sustainability but don’t have the time to follow the full technical process, this summary gives you an evidence-based overview of the Scope 2 update so far, with a particular focus on updates to the market-based method.

I am honoured to have been selected as a Scope 2 Technical Working Group (TWG) member, alongside dozens of global experts. All the slides and minutes from the TWG are posted publicly shortly after each meeting, providing transparency into the process. This blog looks at 7 key messages from the process update based on direct screenshots of key process update documents. For reference, the current Scope 2 guidance for the market-based methods permits the reporting entity to claim the use of clean energy via contractual instruments (e.g, Bundled PPAs, unbundled EACs) that are matched annually to their consumption, and from locations where the claimed power can not actually be deliverable to their load. For instance, in Europe, a consumer in Poland can claim to use Spanish solar to cover their load at nighttime. Current guidance places no other significant limitations on EAC procurement (e.g., incrementality or additionality requirements).

The key takeaway from the update process so far? Granular accounting — aligning clean energy claims with the time and location of actual use — is emerging as the preferred direction of travel for the market-based method across the majority of the Technical Working Group (TWG). This direction of travel is supported by the Independent Standards Board (ISB), which is ultimately responsible for voting on technical updates to the standard. Crucially, the GHG Protocol is an accounting standard to ensure accurate emissions disclosure. It is not a target setting or grading standard and will not require any company to be “zero emissions” or “24/7 carbon-free” by a given date.

But it’s not rigid: there’s also significant flexibility being built into the proposals to support smaller energy users and cases where hourly data is not yet accessible. We are still early in the process, and this blog gives my personal summary of the process to date, not the confirmed final destination. A public comment period will open up in Q4 of this year, and we encourage everyone to make their voices heard when that process begins. The update process and topic are detailed and technical. This blog tries to summarise things to date with 7 key messages. Of course, it is not possible to capture every nuance, so keep that in mind as you read and reach out with any questions.

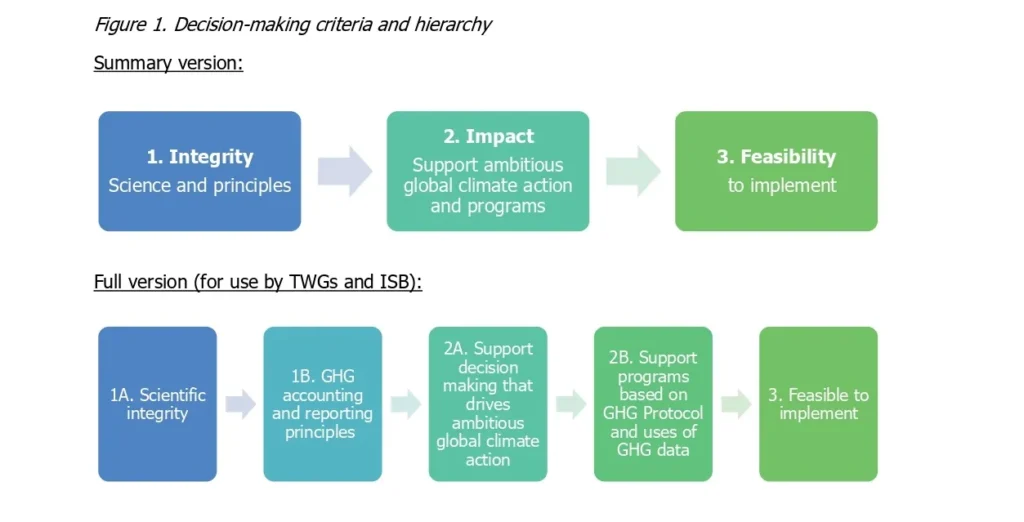

#1: An Integrity-First Governance

Figure 1. Source: GHGP Governance Overview.

The decision-making process for the Scope 2 revision is guided by a clear hierarchy of criteria. First is Integrity, which includes scientific rigor and adherence to established GHG accounting principles (e.g, accuracy, completeness, etc). Second is Impact, emphasizing the importance of enabling ambitious climate action and supporting programs that rely on GHG Protocol data. Third, Feasibility, meaning the protocol should be accessible, adoptable, and equitable, supporting broad, global adoption with efforts made to improve implementation where challenges exist.

Crucially, the GHG Protocol Governance states that “The criteria are ranked in a hierarchy to aid in decision making. When options present tradeoffs between criteria, the hierarchy should be generally followed, such that, for example, scientific integrity is not compromised at the expense of other criteria, while aiming to find solutions that meet all criteria.”

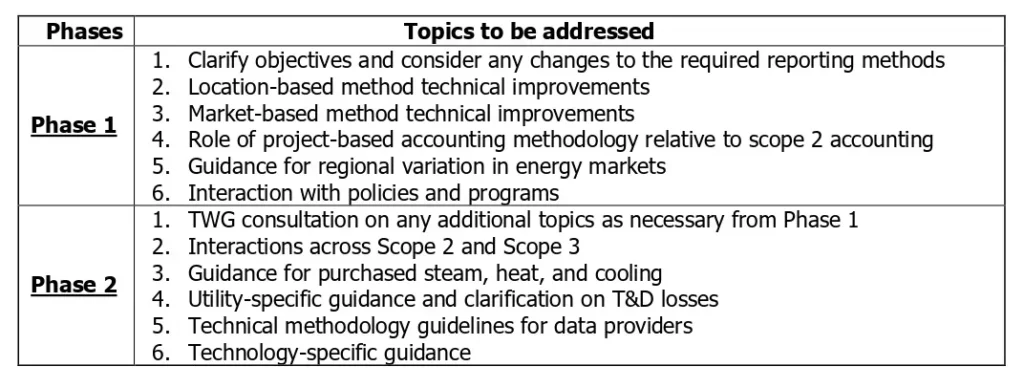

#2: A 2-Phase Process

Figure 2. Source: GHG Protocol – Scope 2 Standard Development Plan.

The Scope 2 update is being tackled in two phases. Phase 1 addresses the core structure and integrity of Scope 2 reporting, including clarifying the objectives, refining both location-based and market-based methods, and exploring how project-based accounting fits into Scope 2. It also aims to provide guidance for regional energy market differences and how Scope 2 interacts with existing policies and programs. Phase 2 will follow up on any unresolved Phase 1 issues and expand into broader technical areas, such as interactions between Scope 2 and Scope 3, accounting for purchased steam, heat, and cooling, and utility-specific topics like transmission and distribution losses. It will also provide methodology guidance for data providers and technology-specific considerations.

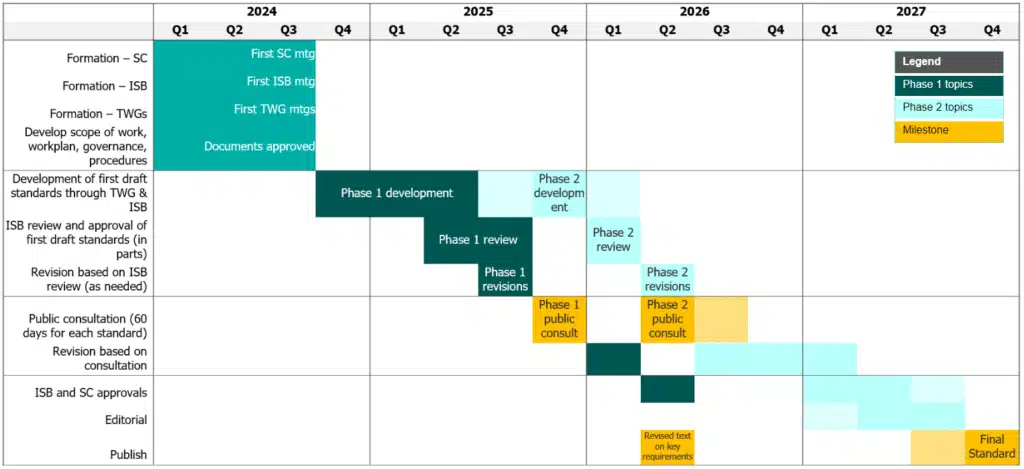

#3: All Roads Lead to 2027

Figure 3. Source: GHG Protocol Scope 2 – Standard Development Plan.

The Scope 2 revision process is unfolding over five years, beginning in 2023 with a survey process and then with the formation of governance bodies and the development of draft content by Technical Working Groups in 2024. Phase 1 revisions are underway in 2025, with the first public consultation expected in late 2025. Phase 2 development runs through 2026, including another review and consultation period. Final approvals and publication are scheduled for 2027. Scope 2 TWG meetings started in Q3 2024, with 14 meetings held to date.

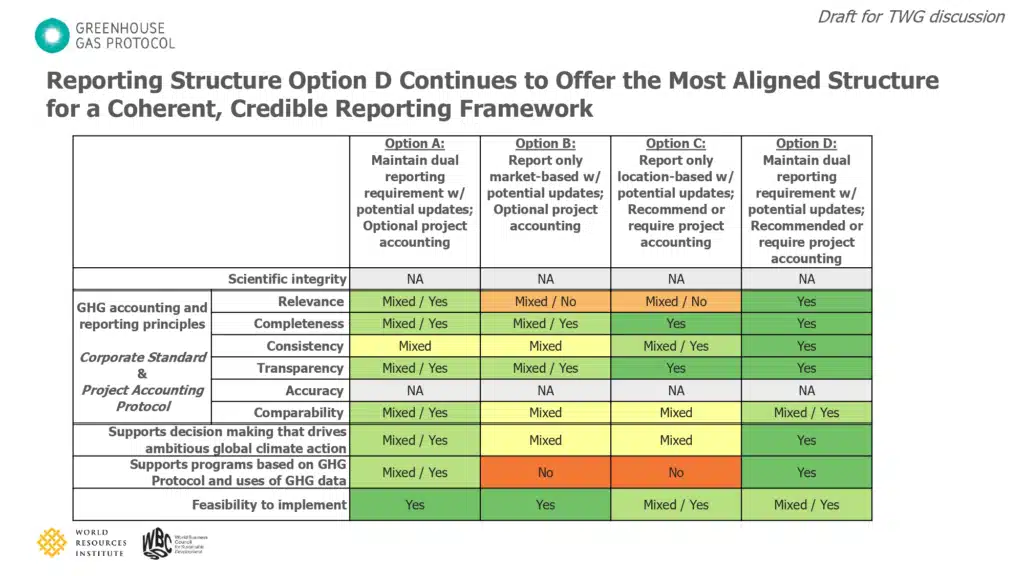

#4: Dual or Tri-reporting

Figure 4. Source: GHG Scope 2 TWG Meeting 12.

One of the most fundamental decisions in the update process is how the overall reporting framework should be structured. The GHGP Secretariat has presented four options, ranging from maintaining the current dual reporting structure to introducing more project-based or refined market methods. The Secretariat’s assessment of how each reporting option aligns with the decision-making criteria identified Option D as the most aligned, receiving consistent “Yes” ratings across key criteria — a view supported by the majority of the TWG. This would see dual reporting of location and market-based Scope 2 inventory numbers remain required, with a potential recommendation or requirement for a third “project accounting” number outside of the Scope 2 inventory. Details still need to be provided about how exactly the project (or “consequential”) accounting number would be calculated. Consequential accounting guidance is being developed by a consequential accounting sub-group of the Scope 2 TWG, and more details are available in the document repository.

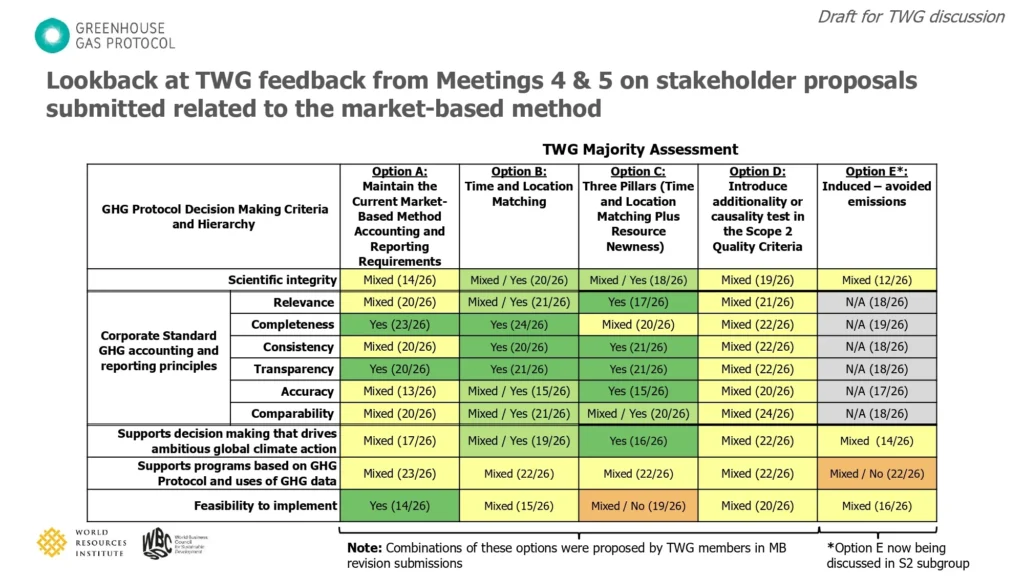

#5: Granular Market-based Accounting Favoured

Figure 5. Source: GHGP Scope 2 TWG #8.

Delving deeper into Scope 2 market-based methods, the table above summarizes polling of 26 TWG members on five different options for the market-based method, as identified in the initial public survey from 2023, based on an evaluation by the secretariat of their alignment with the decision-making criteria. Options B and C — both centered around temporal and location matching — stand out as the preferred choices. They score highest across nearly every decision-making criterion. Option B requires time and location matching, while Option C adds further rigour by tying claims to new clean energy resources. Meanwhile, Options A (status quo) and E (focused on induced/avoided emissions) received notably less support.

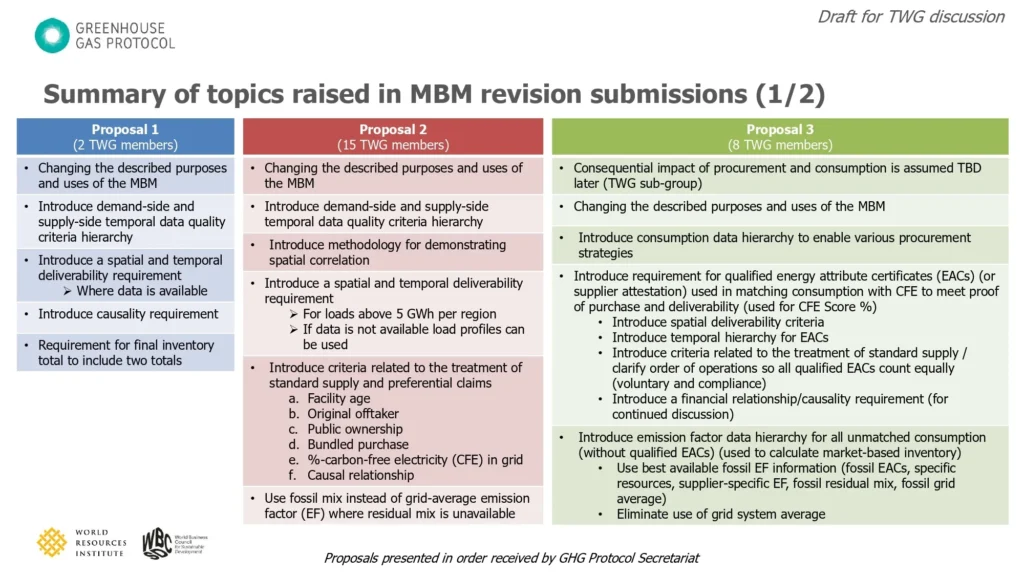

#6: Granular Integrity with Flexibility

Figure 6. Source: GHGP Scope 2 TWG #8.

Based on the five options present above, TWG members with common interests grouped together to develop more detailed proposals, three of which are summarised above, with the three others described in the slides. Proposals 2 and 3 (the ones with by far the most support) outline detailed revisions to the market-based method, emphasizing a shift toward more granular, accurate accounting while building in key flexibilities. Both proposals introduce robust hierarchies for both demand- and supply-side temporal data quality.

A key feature of Proposal 2, backed by 15 members, is the requirement for spatial and temporal deliverability — ensuring that claims are tied to power that could plausibly reach the point of consumption — but with practical flexibilities: aggregate consumption less than 5 GWh per market boundary are exempt from hourly matching, and profile-based estimates may be used when hourly data isn’t available. Proposal 2 also presents various options for the treatment of “standard supply service” (supply paid for by default by the consumer, which will be covered in later blogs) and potential options for preferential claims (e.g., requiring limits on facility age or a causal relationship to the specific generation). While the SSS proposal has received broad support in the TWG, the proposals on preferential claims did not receive broad support. Another flexibility proposal being considered by the TWG is grandfathering long-term contracts signed under the current accounting standard, so companies get credit for any significant financial commitments made before the adoption of any new standard.

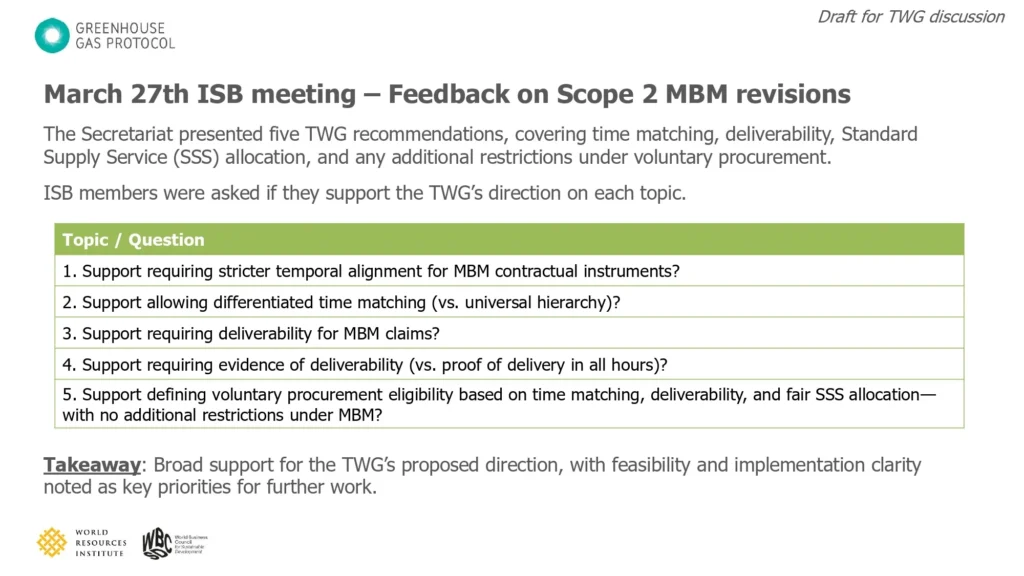

#7: ISB Supports the TWG Direction of Travel

Figure 7. Source: GHGP Scope 2 TWG #11.

Turning to the Independent Standards Board (ISB), which has approval responsibility over the TWG proposal for the Scope 2 standard, we see broad support for the TWG’s proposed direction of travel (i.e., stricter temporal alignment, deliverability, and standard supply service) with feasibility and implementation clarity noted as key priorities for further work.

Next Steps

While the Scope 2 revision process is still in its early stages, a clear direction of travel is emerging — one that aligns with best practices in carbon accounting and growing policy expectations around integrity and transparency. The Secretariat is currently working on a consolidated proposal that reflects the majority view of the Technical Working Group, incorporating the most widely supported elements. Further consultations and refinements are expected as the process moves into its next phase. Stay tuned for upcoming drafts and formal opportunities to engage later this year. Next up, I will do a blog deep dive on the feasibility of the Granular Accounting proposal.