China Built Massive Clean Energy Capacity. What Comes Next?

China’s power sector is getting more complicated. As renewable penetration rises and market reforms move ahead, some of the limits of annual and monthly clean power claims are getting harder to ignore. This is not just a theoretical issue. More and more, the operational and commercial reality of China’s power system depends on timing. Curtailment, negative pricing, and intra-day volatility show up in particular hours on particular days, not neatly averaged across a year. A clean power claim that looks fine over twelve months can still hide a substantial mismatch between when clean electricity was actually generated and when a buyer was using power. As China shifts from rapid buildout to the messier work of integration, that gap begins to matter more.

The practical question is no longer just how much renewable electricity the system can produce over a year, but also whether market structures, procurement practices, and data systems can distinguish between hours when clean power is plentiful and hours when it is tight – and reflect the price difference that comes with that.

Market Design: The Value of Temporal Resolution

China’s market structure is still dominated by mid- and long-term contracting, while spot market reforms are moving at different speeds across provinces. Those reforms are starting to produce clearer time-based price signals, but most buyers still engage with the system through monthly or annual settlement. Thus, there is a disconnect. The system is generating granular operational data, but most procurement and most claims still flatten everything out over a much longer period.

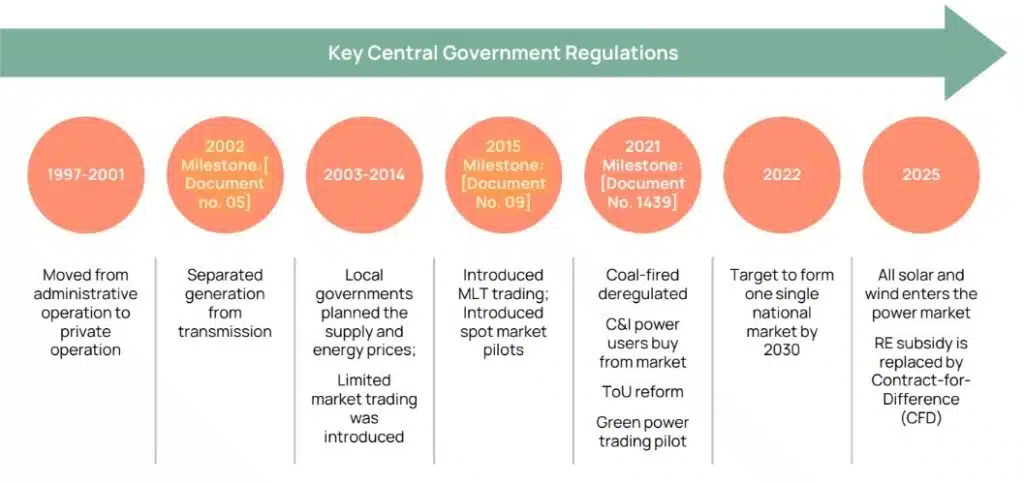

Fig 1: Development and Reform Summary of the Chinese Power Marketю

In practice, a province may already show very obvious hourly patterns of oversupply or scarcity, but buyer-facing contracts collapse those patterns into a single monthly result. That makes it harder for buyers, retailers, and developers to respond to what the system actually needs. It also means a growing share of the signals that really matter, including midday price weakness, evening ramp periods, and curtailment risk, still do not fully show up in how clean electricity is bought, valued, or proved.

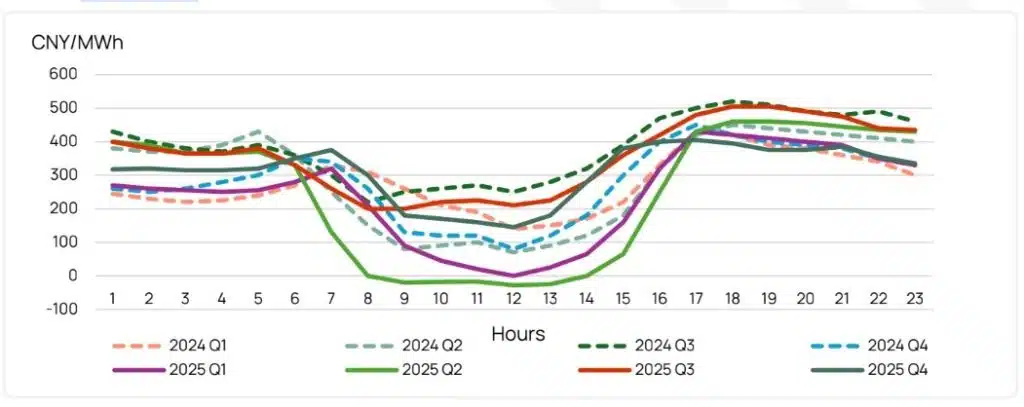

Fig 2: Shandong Day-ahead Spot Market Quarterly Average Prices.

Granular, RTC-style procurement is one way to close some of that gap. By making the timing of both generation and consumption more visible, it allows procurement to line up more closely with system needs and actual price signals. That is especially relevant when the system is dealing with things like midday oversupply, negative spot prices, or insufficient flexibility from storage and other balancing resources. In provinces with high solar penetration, for instance, long stretches of very low or even negative prices are no longer unusual.

Time-resolved contracting and tracking can help push incentives toward the hours when the system is under the most strain. It can also open the door to more differentiated products, not just generic green power, but green power with a clearer sense of when it was delivered, whether it was firmed, and what that meant for settlement outcomes.

For policymakers, that makes granular procurement useful not only as a reporting or compliance tool, but also as something that can support broader market reform, which is still very much in progress in China. For commercial buyers, it offers a route to contracts that better reflect how a high-renewables system actually works, instead of leaning on annual averages that gloss over the challenges.

Exporters and the Shift to Granular Matching

For Chinese exporters, the shift toward granular matching is increasingly being pushed by external requirements. The EU’s Carbon Border Adjustment Mechanism, or CBAM, now requires hourly-matched clean electricity for market-based emissions calculations. Under current retail procurement models, which mostly rely on decoupled monthly contracts, it will be hard to provide convincing evidence of physically delivered, hourly-matched clean power consumption.

Firms that can show this level of granularity will be in a much stronger position to reduce emissions exposure under CBAM and stay competitive in the EU market. That matters because this is no longer only about broad corporate sustainability messaging.

Electricity sourcing is starting to become part of the evidence chain for trade compliance more generally. In other words, power procurement, production records, and carbon accounting are becoming more tightly linked. For export-oriented manufacturers, especially in power-intensive sectors or supply chains that may face carbon audits, being able to show when clean electricity was consumed could become commercially important before granular products are widely available across the domestic market.

CBAM’s compliance rules push electricity out of the background and turn it into a trackable, time-stamped, auditable input for manufactured goods. That has real implications for both market design and data infrastructure in China.

Electricity use, including both carbon content and timing, now needs to be traceable to specific production periods. That is a meaningful shift for policymakers and market participants alike, and honestly not a simple one. It raises practical questions that China’s current market architecture can only answer in part right now. Who can access settlement-grade interval data? How should time-stamped evidence connect to the existing certificate system? What kinds of contracts can support hourly claims? And how should storage, firming, and time-shifting be treated in verification rules? These are not abstract design questions. They are central to China’s ongoing market reforms, its digital infrastructure buildout, and its need to stay competitive industrially.

That is why granular matching matters, not just because it improves the quality of green claims, but because it may shape whether producers can make credible claims in external markets at all.

Implementation: Where the Market Stands Today

China has already started laying some of the groundwork for more granular approaches. Pilots in several provinces have shown that it is technically possible to add time-stamped data to the existing monthly certificate system. But Chinese GECs are still monthly instruments, and access to reliable hourly data is uneven across provinces. Contractual routes for physically delivered, time-stamped clean electricity are also still pretty early. Thus, the question now is not really whether hourly matching can be done, but instead how to scale it in a way that is commercially workable and institutionally credible. The most likely path is gradual rather than sudden. Early momentum will probably come from places like export-oriented industrial parks, large commercial and industrial buyers with advanced metering, and provinces where spot markets are already producing stronger time-based price signals.

A phased roadmap is emerging:

- Start with targeted pilots in provinces with mature spot markets and advanced metering.

- Upgrade registry and data infrastructure to accommodate time-stamped information.

- Develop contracting pathways that support time-bound claims and clarify the treatment of firming and time-shifting.

- Standardise definitions, disclosure guidance, and verification practices across provinces.

- Align domestic evidence and verification pathways to external requirements such as CBAM.

Outlook

The overall direction is pretty clear. As China’s power system becomes more time-resolved in how it operates, there is more value in aligning procurement, claims, and data infrastructure with that reality.

For market participants, that means new opportunities, but also new requirements around contract design, risk management, and export competitiveness.

For policymakers, it reinforces the need for clearer definitions, better data access, and more consistent verification. More broadly, granular procurement should probably be seen as part of market maturation, not some niche add-on. If a system prices electricity by precise time periods, dispatches grid resources in real time, and leans more heavily on flexibility, then procurement and claims frameworks will eventually need to catch up. The closer those layers are aligned, the easier it becomes to reward flexibility, cut down ambiguity around clean power claims, and send better investment signals across the system.

For a more detailed analysis and practical recommendations on RTC clean power opportunities in China’s power sector, see the full EnergyTag/TLG report on China’s Power Sector and RTC Clean Power Landscape. The bigger point here is that China does not have to wait for a fully mature national hourly certificate regime before making progress.

Some next steps are already visible, or at least starting to come into view, including targeted pilots, clearer definitions, better access to spot market interval data, and more explicit treatment of firming and time-shifting in commercial arrangements. None of that solves everything overnight. But it does suggest a plausible path for turning granular matching from an interesting concept into a tool that buyers, regulators, and exporters can actually use. And that will matter in a power system where timing increasingly shapes both operational outcomes and commercial value.

Author:

David Fishman, The Lantau Group